Not Charlie Munger Mindset

Not Charlie Munger Mindset

Different Framing

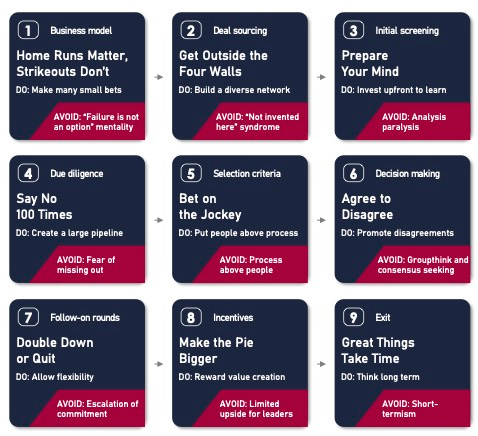

Steve Blank’s blog refers to a book called The Venture Mindset.

It is a book that has compiled anecdotes on how VCs invest, how they think, and how great entrepreneurs build companies. There are reams of blog posts out there already on each of these points.

Charlie Munger was one of the best investors of all time. I learned a lot from him and reading the Berkshire annual letter. When I watched some of this year’s Berkshire Hathaway annual meeting, I was very intrigued by what Warren Buffett had to say about his old partner. Munger was the architect of Berkshire.

They have a style of investing that has beaten the market. Not just by a little. I think there are a few things they do that are similar to the mindset described above, but there are some differences.

One big key difference is the size of the bet. On point one, make many small bets, investors like Berkshire don’t do that. They bet millions. They have to because of the size of their funds. If they make small bets, they don’t get a return.

Of course, another huge difference is Berkshire invests in going concerns with operating profit, operating margin, and some sort of moat on their business.

Venture funds will make smaller bets. However, as an entrepreneur, you must pay attention to fund size when talking to a VC. Why? Because if you are raising $1M and they have a fund size of $1B they won’t invest in you. The check size is too small. Do your homework before you formally ask for a meeting.

When we put together our small microVC fund, we talked a lot about check size and ownership percentage. We looked at statistics. We extrapolated them into the future to see what a successful fund might look like.

I think a lot of VCs make big mistakes in doing this sort of analysis. They write too small a check. If you are a small fund and are only writing a bunch of $50k to $100k checks, enough risk isn’t being assumed.

If you are writing checks like that, you are hoping that every company you invest in becomes a multi-billion dollar rocket ship and the simple fact is there aren’t that many of them. Why are you going to pick it? The strategy of extremely small checks into bunches of companies is like going to the roulette table. It shows a failure to actually understand and contemplate the ideas of risk/reward by a VC fund manager.

Angel investing is different. Yet, the successful angels incorporate and define the 9 principles above in a way that allows them to write smaller checks and be successful.

VC is a risky business. It’s okay to strike out. The key is to know how to establish the strike zone and be very disciplined about it. The variance between the way the venture business invests and the way Berkshire invests is extremely different.

However, failure isn’t fatal in venture. That’s why it seems pretty crass for a firm like Sequoia to say, “We lost 100% on SBF’s fraud, but it won’t affect the fund.” They lost $80MM. It seems like a big number. However, they have a huge fund so all they need is one or two big winners to cover that loss and return the fund.

Of course, fund managers should invest in things they understand.

Berkshire Hathaway, Munger, Buffett v the average VC differ in that the former is investing in going concerns with tons of numbers and management whilst the VC is investing in a bloody startup. Huge difference.

The exit for BH, et al, is a loss on the sale of a stock whilst the VC is usually facing obliteration.

What is common between the two of them is the bet on the people. Buffett is adamant that he invest only with management whose CEO demonstrates integrity. VCs should have the same mindset.

JLM

www.themusingsofthebigredcar.com