GDP=C+G+I+NX

If you haven’t had a classical, and I emphasize the word classical, macroeconomics course, you likely haven’t been exposed to the equation that is used to calculate gross domestic product.

GDP is a measure of a standard of living. GDP expanding means incomes are expanding, productivity is expanding, and the general welfare of society should be getting better. Contraction is the opposite.

In the equation above, C=Consumer; G=Government; I=Investment; NX=net exports. For what it is worth, if you are a classical economist the measure of G is usually 0 or negative. Government spending is a drain on the economy, not a positive. Borrowing by the Feds crowds out private borrowing. People like Robert Lucas challenged the Keynesians, and actually won the argument due to the data and accompanying theory created from his research. Of course, there are Keynesians out there. Larry Summers is one but so are a lot of the talking heads you might see on television. The Keynesians love to play with ISLM curves. Here is a link to the New Keynesian model if you’d like to see it.

GDP isn’t like 2+2=4. It can be subject to interpretation and it is hard to measure. I prefer the classical model due to its simplicity. Professor John Cochrane is a classical economist and has a nice blog post about the relationship between GDP and inflation here.

You will never pin down a macroeconomic professor on absolutes. They always talk in ranges. They speak obtusely. But, the classical guys are more to the point than the Keynesian guys in my experience. Brian Wesbury is far better to listen to than Mark Zandi for an example.

The actions by Trump so far are net negative to GDP in any Keynesian model of the economy. Tariffs should decrease net exports since trade wars are expected to ensue. Decreasing government spending also would send Keynesians into a tizzy, since they put a high positive value on government expenditures. But, they aren’t positive if you are a classical economist either.

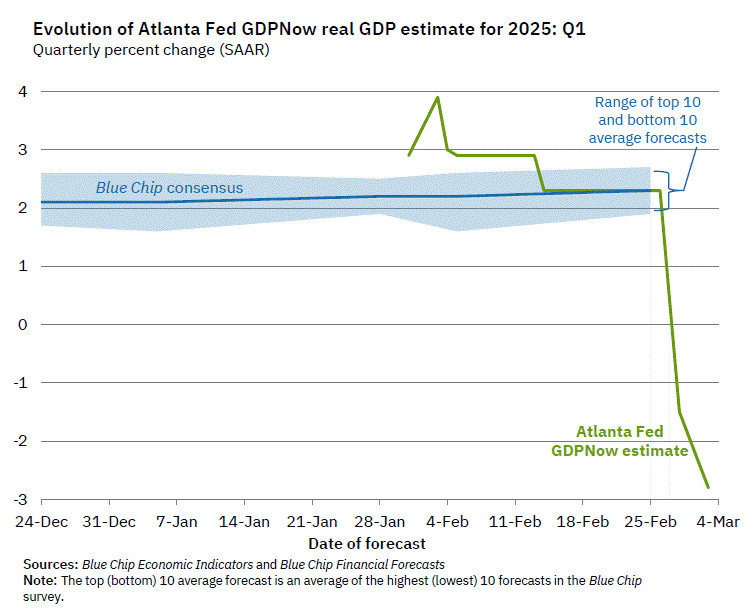

This is what the Atlanta Fed released yesterday. Combine that with 25% tariffs and the market fell out of bed.

There are a lot of Keynesians in the government who work for the Fed. If you remember after the 2008 financial crisis, and the 2020 Covid crisis, the phrase “We are all Keynesians now” was used. I think the estimate of GDP echoes that.

Did the Biden Administration cook the books? Saying this now invites ridicule because critics will say that Trump supporters are making excuses for bad numbers. However, many people suspected Biden was cooking the books. In 2021, the press and Biden people refused to categorize our situation as a recession, even though we were in one.

At the same time, it sure feels like the GDP is not firing on all cylinders. Trump has been President for only a couple of months, and neither House has passed anything of note yet. There is still a fallout from the last Presidency. But markets are forward-looking and price future expectations into today's prices. So, Trump doesn’t get off scot free.

Might we be in another one?

It’s possible for sure. Higher interest rates are slowing the economy. Inflation is not gone, but it’s not as high as it was. Decreasing government spending should cool inflation. There is a lot of uncertainty over taxes and other things, so businesses are not committing. Businesses are the “I” in the classic equation. You can’t blame them for not investing since they are so uncertain about the future.

At the same time, I have seen some animal spirits return, and company merger and acquisition activity is starting to occur.

A friend asked me about Las Vegas yesterday. Vegas can be a bit of a bellwether since coming here is a luxury good. Conventions are crowded. I was down on the Strip last week and it was crowded with conventioneers. Those are booked a year in advance at least. Casino stocks tumbled in the market yesterday. I do know activity on the Strip was down for the Super Bowl. We will see what March Madness is like, but if it’s down, I think you have to say we are in a recession.

Argentina cut government spending and their GDP is booming. The US GDP will not boom by the same kinds of percentages because the base it has to bounce off of is significantly larger. Argentina has been in hand and leg cuffs for 100 years. Economists like Russ Roberts have observed that the US might have done better. We have certainly had some opportunity costs due to bad policy. But, we have done pretty well.

Short term, my guess is we will see interest rates go down….and the stock market not going up until there are some proof points made that what Trump is doing is working. The benefit Trump had in 2016 was that there was eight years of an anemic Obama economy. With Biden, as the market figured out Trump was going to win it rallied so a lot of the bump he might have gotten was already built in. The gas is coming out of the balloon now.

Never catch a falling knife but somewhere in here there will be a buying opportunity.

You are missing one part to that equation- BS- plenty of that to go around over the last 120 years. The unwind of our unconstitutional federal spider web of agencies and hangers-on is going to be initially painful of course. But the graft, and the absolute waste of money that is D.C., nothing takes in dollars and spits out pennies better than D.C. needs to be brought to and end and it won't be pleasant in having the band aid ripped off all at once.

"Never catch a falling knife but somewhere in here there will be a buying opportunity."

The danger isn't in the catching, it's in the trying.