More On The Bailout

More On The Bailout

What If It Was The Right Move?

In principle, I am against bailing out banks. As I said in prior blogs, totally against it in 2008. In principle, I am against the bailout of Silicon Valley Bank, and Signature Bank or any bank. Bankruptcy courts exist, and they are a great disinfectant.

However, I also agree with economist Art Laffer of Laffer Curve fame that a customer who deposits money into a bank shouldn’t have to engage in a credit check on that bank and continue to do due diligence on its financial health while they have money deposited there.

It’s easy to make political points against the banks because of the things they donated to, what their websites looked like, and who was on their Boards of Directors. It’s also easy to demonize the bailouts as bailing out rich VCs. VCs most certainly were bailed out.

Comrade Bernie sounds like Sean Hannity with a different spin. Comrade Bernie would socialize the banks.

It’s hard to ignore the hyperbole. What’s clear is the management teams at those banks were asleep at the wheel and never hedged. That’s basic banking and risk management.

However, what if this is true?

It’s a big deal. It’s also a total abject failure of risk management at all regional banks and we ought to know why that is the case. Why are they using the Alfred E. Neumann School of Risk management to hedge their portfolios?

If most regional banks didn’t hedge and were asleep at the wheel, the Fed did the right thing by stepping in. There would have potentially been a run on regional banks.

It would be nice if everyone came clean and was transparent about it. But, you know that won’t happen and the right and left will continue to chop wood for fuel. It’s funny how SVB was given a clean bill of health by its auditor just a few months ago. They don’t use economic numbers at accounting firms.

I do know this. Peter Thiel was initially the boogeyman for telling startups to pull money but now it comes out that Union Square Ventures in NYC told their startups to pull money out back in November which was way before Thiel. Remember, everyone in the Bay Area detests Peter because he came out as a conservative. They love USV because it leans pretty hard to the left on the political spectrum. It might even be the case that in a Bay Area startup meetup, the founders all decided to move and the word-of-mouth marketing caused everyone to run for the exits. Ted Wright would be proud, sort of.

The answer is it doesn’t matter how the bank went under. If USV told their startups to pull money, they were doing the right thing for those companies, and their LPs. Same with Founders Fund. Same with anyone that told anyone to pull money out.

No one is blaming the bank management teams……wonder why?

By the way, in the market gyrations of the past couple of days, I have noticed an unwinding of the yield curve trade. Haven’t figured out why yet. It’s either deflation starting or we are getting ready for a big reflation. Commodity prices are down across the board and that is one data point. The other thing I will say is we are already in a recession. The only question I am trying to figure out from the yield curve unwind is whether we going into a deeper one, or not.

ADDED FOR CLARIFICATION:

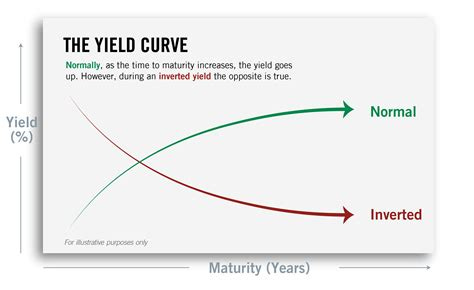

I was asked in the comments to define the “yield curve”. Understand that shop talk gets in the way of communication, so here is a graphic. Kamala loves Venn Diagrams but we don’t do those with the yield curve.

If you look at this, from left to right, the shorter term t-bills are on the left and as you move to the right the “duration” of the financial instrument gets longer. 2 yr note, 5 yr note, 10 yr note, 30-year bond. The bottom axis illustrates that, “maturity” in years.

The vertical axis represents the interest rate paid on that instrument. Hence, shorter duration should equal lower interest rate payments because the risk of holding the instrument is lower. If I give you something and you give me money and I promise to pay you back in a week, the risk should be lower than if I promise to pay you back in a year.

When the yield curve inverts, short-term rates pay more interest than long-term rates OR, the spread between the two rates narrows. Think about behavior: If I am going to pay you the same approximate amount of interest for 3 months as I am 10 years, which instrument do you choose to invest in? Inflationary economies have inverted or relatively “flat” yield curves.

For Silicon Valley and other banks, there are several products they could use to hedge their risk. Deposits come in. They pay out a small interest rate on those deposits, say 1%. The bank can reinvest those deposits into longer-term US T Notes/Bonds and shorter-term US T-Bills. Their very next move should be to go to the CME 0.00%↑ and sell a combination of the SOFR futures, Fed Funds futures, 2/5/10 T-Note Futures, and 30 year bond to match the duration of the portfolio they have created for themselves. That way, if the Fed moves rates higher they lose 0. If the Fed eases rates, they lose on their hedges but they make money on the cash instruments they hold since they should have a higher interest rate value than the current instruments.

This is the first week of Finance 101. Where did I learn it? Not in a classroom but clerking on the CME floor.

Let's be clear as to what an audit is and is not.

An auditor examines the financial statements provided by the company -- PROVIDED BY THE COMPANY -- and opines as to whether they "fairly represent the financial condition of the subject company" as of a certain date.

They do not offer an opinion on the company's business plan or strategy.

They do this by examining in detail about 5% of the accounts which typically entails digging into the general ledger. This work is done by overworked, inexperienced accounting grads as a rite of passage and it is overseen by a partner who rotates on some fixed schedule -- five years.

A good many public companies have a quarterly review and an annual audit. A review is less rigorous than an audit.

Each year the SEC will publish particular areas of emphasis -- the impairment of goodwill as an example -- and require auditors of public companies examine those accounts.

The auditor works from a PBC -- prepared by client -- list of files. If, as example, the SEC asks auditors to examine goodwill impairment then the client will prepare a file on that subject. The more work a company does in preparing good, detailed info for its PBC, the less it costs for the audit.

In the case of goodwill, it would show acquisitions, hard assets acquired, and the analysis of goodwill as a result (the difference between purchase price and hard assets).

If the goodwill is "impaired" -- generally meaning the value of hard assets plus goodwill does not equal some current measure of value -- then the company will propose and the auditor will examine the amount of the goodwill to be expensed as impaired.

When I ran a public company I used to try to write off all goodwill and the auditors would argue that was too much.

The calculation of goodwill impairment is modestly complex with the necessity of creating an applicable unit with some reasonable glue -- all operating units in Texas, as an example -- and analyzing goodwill within the entire unit, not just the latest acquisition.

Of late the SEC has stepped outside its normal practice and asked auditors to examine some odd subjects such as diversity of boards and other seemingly weird accounts. These distractions are not helpful.

If an auditor believes upon the examination of the company's financial statements that the company may fail to exist as a "going concern" they may offer a warning. That is about the only opinion an auditor offers as to operations.

The audit itself is delivered to the audit committee. If there is an area of concern -- a Critical Audit Matter -- the auditor informs the Audit Committee. There are specific rules to follow if fraud is discovered.

The Audit Committee must have a "financial expert" as a member.

If you have a bunch of morons on your Board of Directors, you may have a similarly moronic financial expert on your audit committee and they may have no idea as to what the auditors have discovered. The SVB board seemed a bit light in their loafers and wildly ignorant about banking. They were, however, WOKE AF and they did approve $73MM in support for BLM.

The auditor delivers the audit to the Audit Committee who then gives it to the management who has a chance to reply. This is then subsumed in a SEC filing 10Q (quarterly) or 10K (annually).

Which brings us to the list of required footnotes and disclosures on a company's filings. They are typically the bare minimum to avoid legal liability.

They include things such as shown on this list: https://www.accountingtools.com/articles/what-are-financial-statement-footnotes.html

These footnotes are reviewed for accuracy -- some segment of them -- by the auditors.

A company typically has an investor relations department and a quarterly earnings call both of which will field questions though not ones that require in depth analysis.

All of this is to say, you have to be quite a mechanic to understand these functions and to be able to really glean information from them.

Getting an audit is not something that assures the company knows what it is doing or is doing the right thing.

JLM

www.themusingsofthebigredcar.com

"A wealthy *vulture* capitalist...."

Some idiots I feel sorry for. For Bernie I feel nothing but contempt.

And it's always remarkable how Democrats continuously socialize our problems with these vast government solutions like the ACA yet the problem is never solved. "if you don't have health insurance, but get cancer...." Wasn't the ACA supposed to solve this? Don't people who don't work have access to either Medicaid, or ACA plans with almost their entire premium rebated or free, at the cost to the rest of us? To me, if you don't have health insurance you are negligent, not destitute.

Yet here we are, being harangued once again for something that was supposedly "fixed" in 2010 as one of the biggest pieces of legislation in American history.

Contempt. That's all I feel.