No Credibility

LME Ceases Price Discovery

Markets exist for a lot of reasons, but one of their primary functions is price discovery. Buyers, sellers, and speculators come together in one place and they competitively bid and offer, buy and sell, and “discover” a market-clearing price. If you remember Econ 101, that’s where the intersection of the supply and demand line is.

If you remember deeper discussions in Econ 101, you will remember that price floors, ceilings, and all kinds of artificial rules imposed on markets distort the price.

The London Metal Exchange decided to change all that we know is true about price discovery and free markets. They picked winners and losers.

When the spike in nickel happened, speculators came into the market and sold. Producers sold to lock in their future sales price and profits.

The LME canceled the trades because they were smarter than the market.

This might seem like a small deal to the average person but it’s a big deal. Futures prices ensure that the average person gets goods and services at lower prices than they otherwise would be able to receive them. Futures take a lot of the risk out of production and consumption.

How big is that risk in the nickel market?

Goldman Sachs has started making markets in nickel. The bid price is $25,000 per ton, and the offer price is $37,000 per ton. Usually, these markets would have a spread of $1,000 per ton, not $12,000 per ton. Goldman isn’t making markets out of altruism. They think they can make money, and not just a little.

LME not only canceled the trades, but they also remained closed.

What’s that do to the market? It creates instability in the underlying which you see reflected in the Goldman Bid/Ask. It also allows the losers in the market to accumulate physical inventory, and find financing somewhere. It’s a bail-out to the bad players in the market.

I don’t think he is alone and my hope is other exchanges will open up Nickel futures and compete. CME and ICE are the most probable ones because they can cross-margin through their clearinghouses and bring economies of scale. The one problem they would have is physical delivery, so in the short run, any effort to compete would probably be a cash-settled market. Often in commodities, the players in the market desire a physical settlement because it brings a different sort of discipline.

This is important because we are seeing lots of dislocation and moves in all kinds of commodity markets. The war in Ukraine is going to affect fertilizer prices and the price of grains. Politicians will step in to artificially manipulate the market with programs, price ceilings, restrictions, and all kinds of other maneuvers to try and curry favor with consumers. They shouldn’t. Just let the market sort it out.

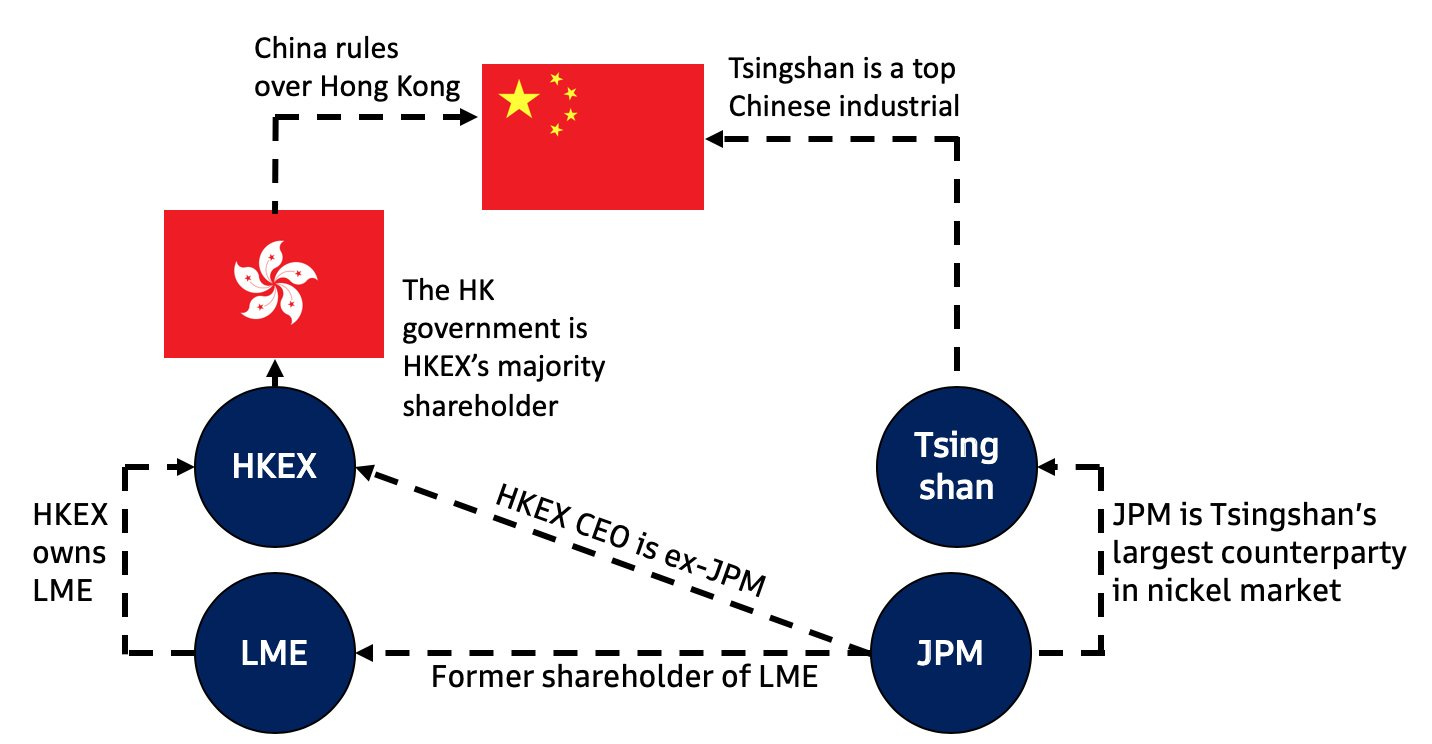

Of course, there is a conspiracy theory with the nickel market but in this case, it might make a lot of sense. It certainly ought to be investigated, and made transparent.

Safe to say the Chinese whale was hooked and punctured, and the LME resuccitated him.

This is not the first time Jamie Dimon’s bank has been involved in turmoil when it comes to the futures industry. Way back in 2011, they were the bank behind Jon Corzine and the fraud he perpetrated on the futures industry.

It’s always funny how smug and proper institutions act until they are going to lose a lot of money.

In this case, if JPM would have been rendered insolvent because of their lack of discipline around regulating the Chinese trader, it’s a good thing for them to go bankrupt.

Markets absorb things like that.

I learned this early in my trading career. I was in the Eurodollar Pit and a friend of mine was one of the largest traders in that pit. He was a huge spreader. He decided he had enough and was going to call it quits. He started trading out of his position, and not adding. That created a void in the market since he was one of the only ones that would assume the risk and trade in certain contracts for big numbers.

Do you want to know what happened the day he left?

Nothing.

Other market-makers stepped up. New market-makers entered the market. Someone else stood in his spot. We just didn’t hear his voice anymore.

The exact same thing would have happened in the nickel market on a larger scale.

If JPM would go under, does anyone care? It’s sort of like a tree falling in the woods with no one around. Does it make a sound?

Yes, there would have been turmoil. But, it would have been resolved very quickly. Markets are like that. They repair themselves pretty quick if we let them.

Except, so many people think they are smarter and bigger than the market.

You might be partly correct

So you obviously don’t know what a merchant bank does for producers

Cash and carry

Or

Hedging commodities

I produce 1 contract of nickel

I hedge 1 contract at lme

Now if I’m a large producer I give my warehouse receipt to jpm they give me a line of credit for the initial margin and will loan me money for variation on the hedge

Basic hedging 101 for commercial entities

Generally in a large squeeze (I have experience with the government on how to break squeezes)

Most banks at a point can’t lend any more money to the client or the exchange raises margins

This is the flaw in futures market

The shorts or hedgers will have to cover

Not the longs they have plenty of cash

You can figure out the rest

Yes much collusion

First the squeezer

Then special interests at the exchange level (Jeff you were one of the only honest guys on the board )

Are to blame

Also incompetence

Like when the cme defaulting on seg funds suing mf global bankruptcy

Btw I found the money for the FBI

So it always isn’t what it seems and the truth nowadays is hard to find .

Great article! Thanks Jeff...as an old econ major, I love seeing how this stuff plays out.