Understanding Markets

Understanding Markets

Markets Are Everywhere, But Few Really Understand Them

Yesterday, Instapundit linked and I thank him. We received a lot of email signups and continue to get them. Hope you sign up too if you like the content of this blog. Share it on social media and with your friends.

When I was trading, there was nothing I loved more than talking about markets with people that really understood them. I used to banter with Leo Melamed about markets. Not where it was going, but the structure and the theory behind them. I’d sit in Bill Shepherd’s office and talk markets all the time.

Then I got into a Facebook fight over the oil market with people that really didn’t understand markets. They wanted to make it all political and they are hard left-wing Democrats (that’s all I seem to run into these days). Republicans want to blame Joe Biden for high oil prices and there is some truth to that, but it’s not really the story. The week Biden was elected, oil was $40 a barrel. Today, it’s $83.98 or $84 per barrel for December delivery. Interestingly, next December’s delivery price right now is $72.38. However, a lot of that cake was baked by things other than Sleepy Joe.

Biden signed executive orders banning exploration, killed the Keystone pipeline, and has revitalized environmental oversight of Big Oil. He did that in the first hours he sat in the chair that occupied the Oval Office. Interestingly, his actions will help the profitability of Big Oil, but hurt the smaller companies in the oil industry. That should sound like a familiar refrain to you because when Big Government enacts Big Policy, it’s medium and small businesses that get hurt. I think the market heard his message loud and clear.

Because the delivery price for next year is lower than it is today mean that Biden’s current policy towards crude oil is going to decrease the price by December 2022?

No.

Markets don’t hinge on one variable, even someone as powerful as the President. Here is what you absolutely need to know and internalize when you try to understand markets. Markets price in all public information and expectations quickly and efficiently. The price you see today reflects that characteristic.

Markets also have costs and opportunity costs. Markets are about allocation of resources, and putting a price on scarcity. There isn’t unlimited demand, nor is there unlimited supply. There just isn’t a free lunch ever when it comes to markets.

President Trump wasn’t the cause of cheaper oil prices despite his claims and what people might say. But, his policies were certainly and decidely more friendly to the oil industry and the price reflected it. Expectations of a more elastic supply line, and an expanding supply line were reflected in the price.

During the Trump administration, futures prices for oil went NEGATIVE for a while. That wasn’t because of Trump’s policy. It was because there wasn’t enough storage capacity for oil. We had too much supply!

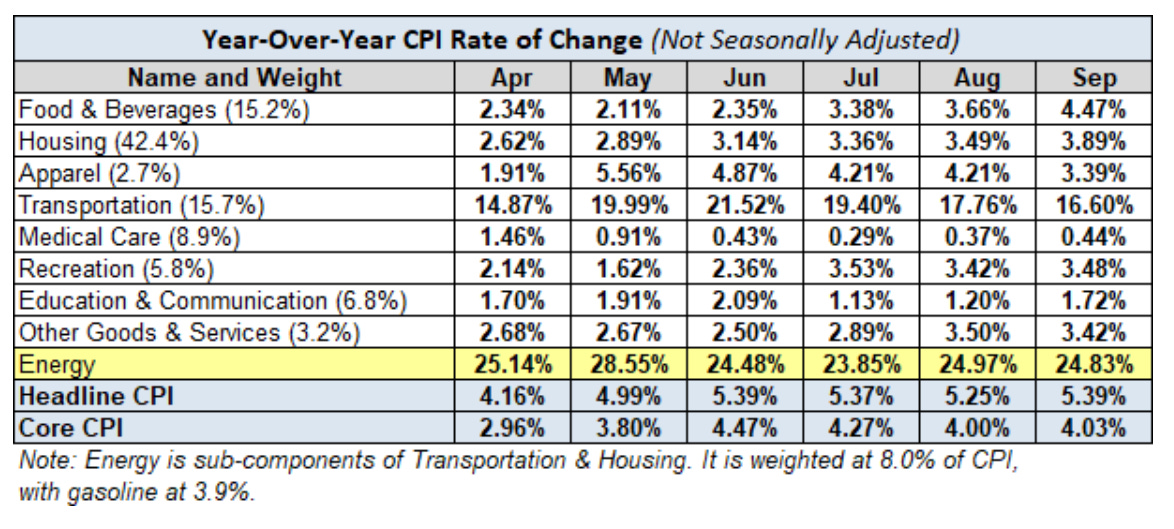

Here is the latest chart on all prices courtesy of my friend Jeff Minch.

All markets look at that and price those numbers into today’s price. You might say, “Well, that’s speculative”, and you would be right. But, speculators alone don’t drive prices. If you look at recent oil supply reports, production is down. That means supply is down with demand unchanged. Prices have to go up.

As a matter of fact, if you took away the speculators in markets, the actual bid/ask spread between buyers and sellers would increase making markets more volatile and causing prices to go higher, or lower when they trend down, than they should be.

Mostly when I see people grouse about markets they are ticked because their preferences aren’t being reflected in what is going on. It’s impossible for them to step back and be objective. They want to be benevolent dictators and decide what’s best for everyone else. They fall into the same trap central planners fall into that they know better than a group of independent buyers and sellers trading at arms length.

You might wonder, “Why don’t oil companies produce more if the price is higher? They have an incentive to do so? Isn’t the market sending them that signal?” You’d be correct again. Except, what besides price might influence their decisions on production? Hmmm, wonder if I could put my finger on that one?

Every market participant, bull or bear, factor in the tenor of public policy when it comes to markets. It isn’t the dominant variable, but it’s a variable. The more the Big Guy in the Oval Offices jaws about fossil fuels, the more looming that variable becomes. Why? Because it enables his underlings to aggressively attack the companies in the oil industry. Maybe it is not an EPA violation, but an audit from our friends at the IRS. Maybe it’s not some new environmental regulation, but perhaps the Commerce Department decides that they don’t want to see some acquisition go through.

Once when I was doing political stuff at CME, Congressman and House Financial Services Committee chairman Barney Frank came to town to talk about regulation of commodity markets. He was really ticked about the price of oil. Oil had rallied to $140 per barrel or something like that. He wanted to regulate the price of oil and determine it by fiat. Barney didn’t understand markets.

For what it is worth, President Richard Nixon didn’t understand them either. His wage and price controls of the early 1970s were terrible government policy that had big consequences down the road. Same with FDR and his schemes in the 1930s and early 1940s. No faith in markets.

The other massive issue that all commodity markets have today is the shut down of the economy and continued Covid policies to combat it. Supply chains cannot catch up. Alex Berenson has a lot of data on the failure of lockdowns and the failure of the vaccine here. As he says, “virus gonna virus”.

Vaccine mandates cause people to leave their jobs.

Work from home and draconian state policies have caused people to leave their jobs.

Government policies have dampened incentives for people to go get new jobs.

Under Trump, government was pro-energy. Under Biden, it’s decidely anti-energy.

The reason to pay very close attention to the energy sector is it influences lots of other sectors. For example, if you wonder why your bowl of cereal is costing you more, it’s not just because of supply chain constraints. It’s also because of Federal government ethanol policy. Grain trade watches energy prices move higher, and acts accordingly.

Many people wonder why energy companies aren’t investing in new supply with prices so high. It’s because the incentive is gone. There are opportunity costs to government policy.

Energy companies have been paying executives more, buying back stock, increasing worker salaries and increasing dividends. What else would they do with the excess cash? When it sits on balance sheets it makes them a takeover target, and with low levels of interest being paid on debt, there is no incentive to park it in debt instruments.

Of course, with the rate of inflation increasing as it has people who are getting raises are going to become victims of bracket creep. Workers will earn more money, but inflation is also running hot. That means even though they received a raise, their money doesn’t go further. In addition, with the higher income they are receiving, they often get bumped to a higher income tax bracket. The increase in income has them paying more taxes than they used to pay. That decreases the incentive to work at a time when companies are hurting for workers. Fun times!

Economist Mark Perry has said, “markets in everything”. He’s right. Human incentive is to find the best quality, or in economic terms “most utility”, at the cheapest price. Humans are hard wired to trade and divide labor. That creates all kinds of markets. Every single decision you make has an opportunity cost.

The beauty of a market based economy is that it lets buyers and sellers come together to trade. The transparent price that is created from that trade causes people up and down the supply chain to make decisions. Those decisions are incorporated into the price of the market and cause new decisions to be made. It is a virtuous circle.

The end result is you get your goods and services at the cheapest price you can. Thanks to the market, people have an incentive to innovate, do things better and faster, and raise standards of living for themselves and everyone.

The alternative isn’t pretty.

"The alternative isn't pretty"

A guy named Gennady Andreev-Khomiakov served as Deputy Manager of a Stalin-era factory. The General Manager was a very sharp guy, and many improvements were made, but the factory (a lumber mill) was being strangled by inability to procure adequate supplies of raw lumber. Gennady, whose father had been in the lumber trade before the revolution, was contemptuous of the chaos into which the industry had been reduced by the Soviets:

"The free and “unplanned” and therefore ostensibly chaotic character of lumber production before the revolution in reality possessed a definite order. As the season approached, hundreds of thousands of forest workers gathered in small artels of loggers, rafters, and floaters, hired themselves out to entrepreneurs through their foremen, and got all the work done. The Bolsheviks, concerned with “putting order” into life and organizing it according to their single scheme, destroyed that order and introduced their own–and arrived at complete chaos in lumbering."

As Gennady says:

"Such in the immutable law. The forceful subordination of life’s variety into a single mold will be avenged by that variety’s becoming nothing but chaos and disorder."

His book, 'Bitter Waters', is well worth reading.