Well Oiled Angel Groups

How They Should Work

A younger friend of mine Jackie DiMonte has a venture fund based in Austin, Texas. She’s from Chicago and she worked the circuit of VC in Chicago before leaving to start her own fund in Austin, Texas.

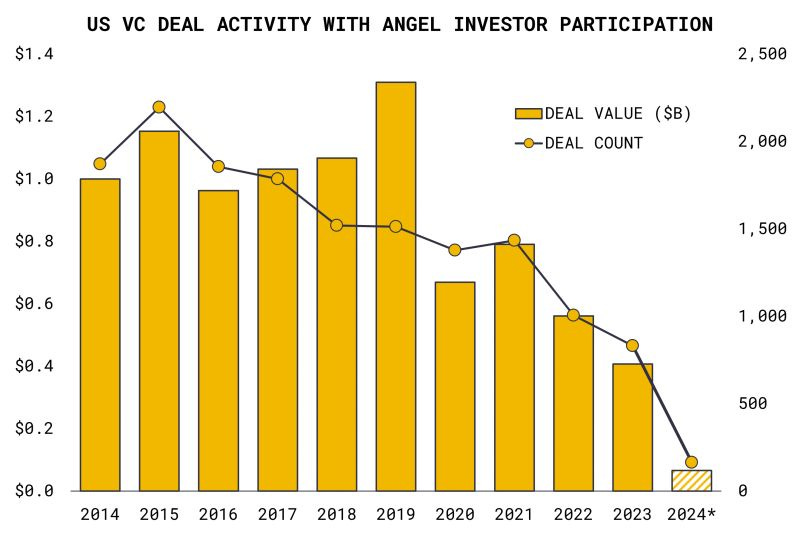

She’s smart and you’d be lucky to have her as an investor if your company and her VC fund can get together. Her Linked In is very thought-provoking. She posts a lot of venture data that is interesting to think about. Her latest post was on the fall off of financing from Angel groups.

As a person who started an angel group, I find this really interesting and while there are no surefire clearcut answers to why this pattern is persisting the speculative answers are ripe for discussion and probably pretty close to what is going on. An academic would have to research it to really find out. “It works in practice, but does it work in theory”.

It is kind of mind-blowing as Jackie points out. Let's think about the traditional allocation of startup capital. Angels generally invest the same amount as venture capitalists in the first round of funding when it comes to gross dollars. That data has repeated itself over decades at both PitchBook and at the Angel Capital Association.

Why it is happening gives us some insights. What if anything should we do about it? Does it matter to the startup community in general and because startups are the lifeblood of innovation which raises the standard of living for us as a people, does it matter to us as a country or civilized society?

Heavy stuff.

More specifically, how should a well-oiled angel group function and operate? How does it get great deal flow and get into deals?

First things first. There are several reasons I think angel participation is down:

The economy stinks. When the economy stinks, investors pull back.

Inflation. People have to allocate money to live, not to luxury investments like startups.

The rise of many small pre-seed funds. I hypothesize that many angels might have outsourced the job to invest in startups to small fund managers. That’s how they have decided to get exposure to startups. It makes some sense because if you want to be successful at angel investing it takes commitment and work. Angels have to look at it like a job, not a hobby.

Returns in the stock market over the last several years have been uneven, but better than the returns to venture investing. There are costs and opportunity costs to angel investing. One huge cost is the liquidity premium you pay by investing in a startup. That demands an outsize projected 30x return. Last year and in 2022, the S+P 500 had a nice return after a dismal 2021. No liquidity issues. Additionally, the interest you can earn risk-free is significantly higher today than it was in the years 2014-2021.

Valuations at pre-seed and seed stages ramped up exponentially between 2014-2022. I am so old I can remember doing seed deals at a $4MM pre-money. In our fund, we were highly disciplined about valuation and ownership percentage.

Because of the run-up in valuations, angels have to write larger checks to get similar ownership. There is a gigantic difference in outcomes between writing a $25k check at a $5MM pre-money and a $25k check at a $10MM+ pre-money. The place a company has to target an exit opportunity for the investor to earn an outsize return is vastly different as well. It’s like a bullwhip effect and the difference is not linear.

Companies are staying private longer and delaying liquidity events. That turns off angel investors.

Behavioral economics. If I started investing in 2016, I saw a large run-up in the valuations of many companies I put money into. Today, we are seeing down rounds and less of a markup on valuation. Behavioral economics has proven that losses hurt a lot more than winners feel good. It’s about 4x the pain. That’s caused investors to pull back. VCs also pulled back in 2021.

Angel groups have pulled back. They are trying to invest later in the cycle to derisk investment. Of course, this is the antithesis to why angel investing was started but as angel groups have tried to institutionalize themselves, they lost their core mission.

The population is aging. The youngest baby boomers are 60. Baby boomers hold most of the wealth that can find its way into riskier investments like startups. Investing in a portfolio of startups at age 60 looks a lot different than at age 40. Why? Liquidity, and time to exit. Do you want to be babysitting startups until age 80?

What does it mean? Hard to say. If the dollar going into early-stage startups is static, or higher does it matter if it comes from funds or angels? We ought to be indifferent. I do think that the United States has a vested interest in seeing private dollars flow to early-stage startups to spur innovation. It increases competition. It raises standards of living when they are successful. It makes the US a magnet for high-quality people and a magnet for risk-loving investment dollars.

Angels can have different relationships with founders than funds. Funds might be indifferent when a company struggles. They have other deals they will do. Angels might not be. It might be one of their only investments. Additionally, maybe the angel invested because they have a specific skill set and network to bring to bear to help the company succeed. They can energize that network more easily than a fund might be able to.

Angel groups cannot succeed everywhere. Generally, you need a few things to be successful. The first is population. Setting up a group in BuFu nowhere is going to make it hard to be successful. More population generally means more money. Can’t have an angel group without people who can afford to invest. You will need to recruit them and in that process, for every ten people you speak with maybe one will say yes. A second beneficial feature of success is to be located near a great research institution. They tend to spin out a lot of entrepreneurs. I love Grand Marais, Minnesota but setting a group up there would be setting yourself up for failure. Duluth, MN as well. Minneapolis, you get a chance depending on what you want to invest in and how.

Investing in something that local people know helps a lot. I spoke with some people in Madison, Wisconsin a number of years ago about setting up an early stage investing fund. They wanted to do “heavy tech”. Sounds great except that was already being done at scale in places like Silicon Valley. They pursued it, and the effort failed. If they would have pursued agriculture, water, healthcare (Epic is near there) they might have done pretty well.

There are a lot of angel groups in the US. Not all of them function well. Some really don’t do much at all. Given my experience, I have some real general principles that I think make angel groups work well.

Automation with software. Companies like Carta should form the backbone of aggregating capital and reporting how that capital is performing. Carta can form your SPV, do the tax, and each angel has an individual account so they can login on their own and see how investments are doing. We used Carta at our fund and it really made life a lot easier.

Whoever leads the group has to be a facilitator. They need to act like an air traffic controller or golf caddy. They are mostly a supporter and let other individual angels shine. They need to know where the resources are and match them up to the right people to get things done.

Angels have to be empowered to find deal flow and bring it to the group. The group can have a formal portal, but individual angels should be able to circumvent the portal and bring deals in.

Angels should do the diligence. They should collaborate. If you did a good job recruiting angels, you have a group that has a diverse set of business experiences. In this age of “diversity is good” I hasten to point out that the prior point has zero to do with gender, color, sexual orientation or anything like that. Engineers think differently than financiers and corporate people think differently than entrepreneurs. It’s through objective analysis, sharing of experience, and honest discussion that you suss out the best deals. Outsource your diligence and you outsource returns.

Diligence should have a standardized process that everyone understands. At the same time, it needs to be fast and efficient. From the time an entrepreneur applies to the time they get back a “no” should be no longer than a couple of weeks. A “yes” takes longer but the group should be 200% transparent with the entrepreneur how it operates and what is going on. Empowered angels can do that for you because they often become the deal champion.

Angel groups need a standardized process and cadence of meeting physically together. “We meet 6 times a year.” However, this is where the leader of the group becomes a facilitator. Great deals don’t show up 6 times a year. They happen randomly. The leader needs to be able to work outside the process to get a deal done. It’s important that they are a great communicator, and are transparent so angels don’t feel like they are left out.

Angel groups need to understand their role and their lane. They are not funds. Some groups might have sidecar funds, but the group itself isn’t a fund. Don’t act like one or operate like one. Angels invest EARLY. Groups that try and initiate further down the investment stack will find they cannot get into the best deals.

Angel groups ought to have some sort of thesis around investing to help them sift deal flow and to indicate to the community how they invest. In the group I started we invested in what Chicago was good at, and no more than a day’s drive away. We had four groups that specialized in finance, healthcare, consumer products, and industrial B2B.

Angel groups can do a lot for the broader community by educating it. Show up at high schools, community colleges, and colleges and talk about investing. Do local office hours and see who shows up to chat. It should not just be the leader of the group that does it.

Angel groups should have Boards of Directors. That board ought to be term-limited to get new people in and to stop people from trying to build power centers within the group.

The leader of the group ought to also have a term limit. Change in leadership is not a bad thing. This encourages mentorship within the group. Situations change, economies change, and so the group has to be flexible enough to prepare for it.

Angels can add a lot of value to companies. I have seen it happen. I have seen an angel take a company under their arm and really add value, more so than a lot of funds. If you do the angel job correctly, you can make decent money and outsize returns. Do it wrong, you get a lot of write-offs. Get with a bad group, it’s not fun. Angel investing ought to be fun.

It would be interesting to see how the chart tracks with the cpi. Inversely, I bet it would track pretty close. Another interesting chart would be how it tracks with consumer debt. The reason I think these comparisons would be interesting is that so much if this is psychological. If a few key VC’a stop investing, most others will as well. If I’ve learned anything from investors like Warren Buffet, do the opposite of what the herd is doing. Especially if they are going off the cliff. Maybe these VC’s are wise enough to see the herd headed off the cliff. My other theory is that the US dollar has lost significantly more value, psychologically, than is reflected in quantifiable data. If this is true, we will begin to see signs of significant increases in the prices of gold and silver soon.

I think the decrease in VC activity is due to demographics too. For the next 15 years the economy will be concerned with the preservation of wealth and the burgeoning national debt to finance the final years of the Baby Boomers. The investor's time horizon is too short.